Summary

Many successful wealth builders prioritize cash flow management before pursuing investments or aggressive financial strategies. Consistent positive cash flow provides stability, reduces financial stress, and creates the foundation for long-term wealth creation. By controlling spending, optimizing income, and directing surplus cash strategically, individuals can build sustainable financial growth while minimizing debt and financial risk.

Understanding Cash Flow: The Foundation of Financial Stability

When people think about building wealth, they often picture investing in stocks, real estate, or starting a business. While those strategies can certainly contribute to long-term prosperity, many experienced financial planners emphasize a simpler starting point: cash flow management.

Cash flow refers to the movement of money in and out of your personal finances. Income from salaries, side businesses, or investments represents inflow, while expenses such as housing, groceries, transportation, and debt payments represent outflow.

A positive cash flow occurs when income consistently exceeds expenses.

This concept may seem basic, but its importance cannot be overstated. Wealth builders often focus on cash flow first because it determines whether someone has the capacity to save, invest, and absorb financial shocks.

According to the U.S. Federal Reserve’s Survey of Consumer Finances, households with steady surplus cash flow are significantly more likely to accumulate assets and less likely to rely on high-interest debt.

Without control over cash flow, even high-income earners can struggle financially.

Why Cash Flow Matters More Than Income Alone

Many Americans assume that higher income automatically leads to financial success. In reality, income is only one part of the equation.

A household earning $200,000 per year but spending $210,000 annually will accumulate debt. Meanwhile, someone earning $75,000 while consistently saving $10,000 per year may steadily build wealth.

Cash flow reveals the true financial trajectory.

When financial advisors review a client’s finances, they usually begin by analyzing monthly inflows and outflows. This provides insight into spending patterns, lifestyle costs, and potential areas for improvement.

Key benefits of strong cash flow management include:

- Consistent savings capacity

- Reduced reliance on credit cards and loans

- Greater ability to invest regularly

- Financial resilience during emergencies

- Improved long-term planning flexibility

Many wealth builders treat cash flow as the engine that powers every other financial strategy.

Cash Flow Enables Consistent Investing

Investing is widely recognized as a powerful wealth-building tool. However, investing requires one essential ingredient: money available to invest.

Positive cash flow creates that opportunity.

When someone consistently spends less than they earn, the remaining surplus can be directed into:

- Retirement accounts such as 401(k)s or IRAs

- Brokerage investment accounts

- Real estate purchases

- Business ventures

- Debt reduction strategies

The power of this approach lies in consistency.

For example, a professional who invests $500 per month starting at age 30 may accumulate hundreds of thousands of dollars over time due to compound growth. Without reliable surplus cash flow, those regular investments are difficult to maintain.

Wealth builders often focus on strengthening their financial base first so that investing becomes automatic rather than sporadic.

Cash Flow Management Reduces Financial Stress

Financial stress is a common challenge for many households.

According to the American Psychological Association, money remains one of the leading sources of stress for Americans year after year.

Much of that stress stems from unpredictable finances—months where expenses exceed income or where unexpected costs disrupt the budget.

Managing cash flow helps create predictability and stability.

When individuals track their expenses and align spending with income, they gain greater visibility into their financial situation. This clarity allows for better planning and fewer unpleasant surprises.

For instance, someone who understands their monthly spending habits can plan ahead for:

- Annual insurance payments

- Holiday spending

- Medical expenses

- Vehicle maintenance

- Tax obligations

Rather than reacting to financial problems, they proactively prepare for them.

The Role of Cash Flow in Debt Reduction

Debt can significantly hinder wealth-building efforts.

High-interest credit cards, personal loans, and other liabilities consume income that could otherwise be invested or saved.

Effective cash flow management provides the structure necessary to reduce and eliminate debt.

When someone identifies a monthly surplus—even a modest one—they can apply that surplus toward accelerated debt repayment.

Common strategies include:

- The debt snowball method, which focuses on paying off smaller debts first

- The debt avalanche method, which prioritizes high-interest balances

- Consolidation strategies to reduce interest costs

Once debt obligations decline, the freed-up cash flow can be redirected toward savings and investments.

This transformation—from debt payments to asset building—is one of the most powerful shifts in personal finance.

Cash Flow Supports Emergency Preparedness

Unexpected expenses are inevitable.

Job loss, medical issues, home repairs, and car breakdowns can all disrupt financial stability. Households without adequate savings often rely on credit to handle these events.

Positive cash flow allows individuals to gradually build an emergency fund.

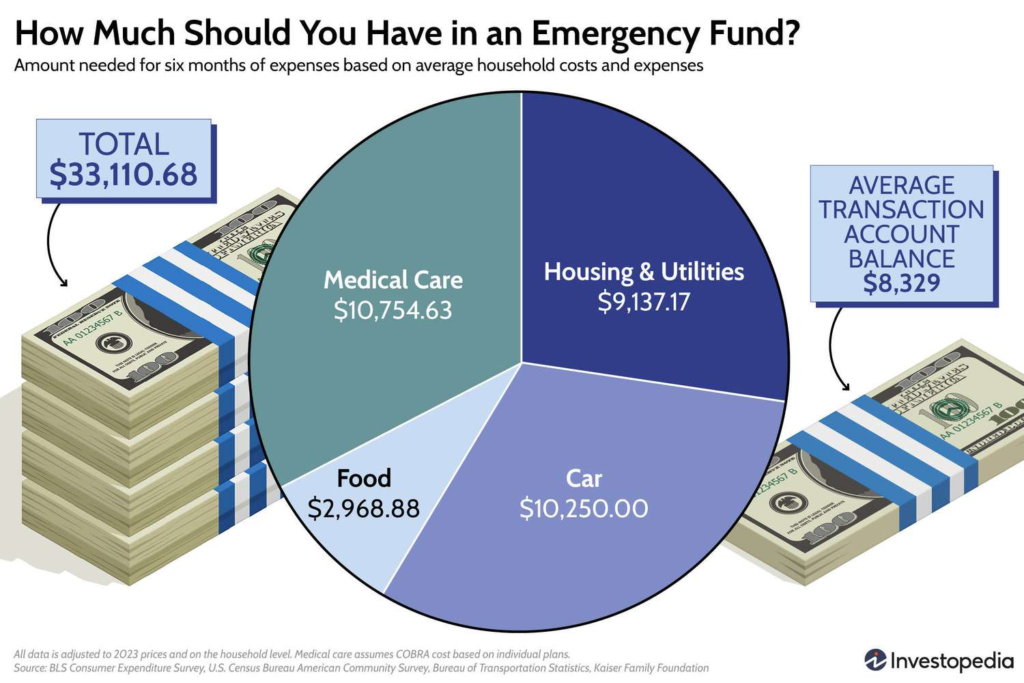

Financial planners typically recommend maintaining three to six months of living expenses in accessible savings.

Building such a reserve takes time. Consistent surplus cash flow makes it achievable.

Consider the difference between two scenarios:

- A household living paycheck-to-paycheck

- A household saving $400 per month

Within two years, the second household may accumulate nearly $10,000 in emergency savings. This buffer dramatically reduces financial vulnerability.

Real-World Example: Two Different Financial Paths

To understand the importance of cash flow, consider two hypothetical professionals with similar salaries.

Case 1: High Income, Poor Cash Flow

Emily earns $120,000 per year but spends heavily on lifestyle upgrades—luxury apartments, frequent travel, and expensive dining. Her monthly expenses exceed her income, and she carries significant credit card balances.

Despite her high salary, she struggles to save.

Case 2: Moderate Income, Strong Cash Flow

David earns $80,000 annually but carefully manages his expenses. He maintains a modest lifestyle and consistently saves $1,200 per month.

Within five years:

- David has built a substantial investment portfolio.

- Emily has accumulated debt and little savings.

The difference is not income—it is cash flow discipline.

Practical Ways to Improve Cash Flow

Improving cash flow does not necessarily require drastic lifestyle changes. Often, small adjustments produce meaningful results.

Common strategies include:

- Tracking monthly expenses for greater awareness

- Negotiating recurring bills such as internet or insurance

- Reducing unused subscriptions

- Increasing income through side work or career advancement

- Automating savings transfers immediately after payday

Many wealth builders view cash flow optimization as an ongoing process rather than a one-time exercise.

Even small improvements—an extra $200 saved each month—can significantly impact long-term financial outcomes.

Technology Is Making Cash Flow Management Easier

Modern financial tools have simplified the process of tracking and managing personal finances.

Budgeting apps and digital banking platforms allow users to monitor spending, categorize expenses, and visualize financial trends in real time.

These tools can help individuals:

- Identify overspending categories

- Set spending limits

- Automate savings goals

- Monitor subscription charges

- Forecast future cash flow

For many people, visibility alone leads to better decision-making.

When spending habits become transparent, it becomes easier to align daily financial choices with long-term goals.

Why Experienced Investors Still Prioritize Cash Flow

Even individuals with substantial investment portfolios continue to pay close attention to cash flow.

Real estate investors evaluate rental properties primarily based on cash flow potential rather than appreciation alone.

Business owners monitor operating cash flow to ensure their companies remain financially healthy.

Retirees rely on predictable income streams—from pensions, dividends, or annuities—to support their lifestyles.

Across these scenarios, the same principle applies: sustainable wealth requires reliable cash flow.

Assets may fluctuate in value, but steady income relative to expenses provides lasting stability.

Frequently Asked Questions

Why is cash flow important for building wealth?

Cash flow determines how much money is available for saving, investing, and paying down debt. Without surplus cash flow, it becomes difficult to accumulate assets over time.

Is budgeting the same as cash flow management?

Budgeting is one tool used to manage cash flow. Cash flow management focuses more broadly on tracking income and expenses and ensuring inflows exceed outflows.

How much positive cash flow should someone aim for?

Financial planners often recommend saving at least 15–20% of income when possible, though even smaller percentages can make a meaningful difference over time.

Can someone build wealth without strong cash flow?

It is possible but much harder. Without consistent surplus income, individuals may rely on irregular financial gains rather than steady wealth accumulation.

What are common signs of poor cash flow?

Common indicators include living paycheck-to-paycheck, increasing credit card balances, difficulty saving money, and frequent reliance on loans to cover routine expenses.

How can someone increase cash flow quickly?

Reducing discretionary spending, renegotiating recurring bills, and temporarily increasing income through side work can improve cash flow relatively quickly.

Should debt repayment or investing come first?

Many financial experts recommend eliminating high-interest debt before focusing heavily on investing, since interest costs can outweigh potential investment returns.

How does inflation affect cash flow?

Inflation increases the cost of goods and services, which can reduce surplus cash flow unless income rises proportionally.

Is cash flow management different for freelancers or business owners?

Yes. Irregular income requires additional planning, including larger emergency reserves and more conservative budgeting.

Do wealthy people still track their cash flow?

Many do. Even high-net-worth individuals monitor inflows and outflows to ensure their financial strategies remain sustainable.

Building Wealth from the Ground Up: The Cash Flow Mindset

Long-term financial success rarely begins with complex investments or risky financial bets. Instead, it often starts with something far simpler: understanding and controlling the movement of money.

By prioritizing cash flow management, individuals create the financial stability needed to invest consistently, handle emergencies, reduce debt, and pursue meaningful financial goals.

Wealth building is not only about how much money you make—it is about how effectively you manage the money you keep.

Key Insights at a Glance

- Positive cash flow forms the foundation of sustainable wealth

- Income alone does not determine financial success

- Surplus cash flow enables consistent investing

- Debt reduction becomes easier with improved cash flow

- Emergency savings depend on reliable financial surplus

- Technology has simplified financial tracking and planning

- Wealth builders across industries prioritize cash flow stability