Summary

The Federal Reserve plays a powerful but often invisible role in Americans’ everyday finances. From mortgage rates and credit cards to job markets and savings accounts, the Fed’s decisions shape borrowing costs and economic stability. Understanding how Federal Reserve policy works can help households make smarter financial decisions, anticipate economic changes, and better manage debt, savings, and long-term financial planning.

Why the Federal Reserve Matters to Everyday Americans

Many people hear about the Federal Reserve in news headlines but assume it mainly affects Wall Street or government policy. In reality, decisions made by the Federal Reserve System influence nearly every American household.

The Fed is the United States’ central bank. Its primary responsibilities include:

- Managing inflation

- Promoting maximum employment

- Maintaining stable financial markets

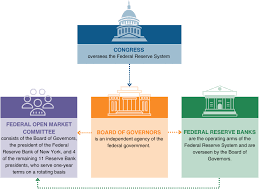

These objectives—often referred to as the Fed’s dual mandate—guide the actions of the Federal Open Market Committee (FOMC), the group responsible for setting interest rate policy.

While these goals may sound abstract, the policies used to achieve them directly affect the cost of borrowing money, the return on savings, and the stability of the broader economy. When the Fed changes interest rates or signals future economic policy, banks, lenders, investors, and businesses adjust their decisions almost immediately.

For households, that means the Federal Reserve influences everything from monthly mortgage payments to job opportunities.

How Federal Reserve Interest Rates Influence Your Wallet

The most visible tool used by the Federal Reserve is the federal funds rate—the interest rate banks charge each other for overnight loans.

Although consumers rarely interact with this rate directly, it forms the foundation for many other interest rates across the economy.

When the Fed raises interest rates, borrowing becomes more expensive. When it lowers rates, borrowing becomes cheaper.

This shift affects several areas of personal finance.

1. Mortgage Rates

Mortgage rates are heavily influenced by long-term Treasury yields and expectations of future Fed policy.

For example:

- When the Fed increases rates to fight inflation, mortgage rates often rise.

- When the Fed cuts rates to support economic growth, mortgage rates tend to fall.

According to data from Freddie Mac, average 30-year mortgage rates in the United States rose above 7% in 2023 during aggressive Fed rate increases, significantly raising monthly payments for new homebuyers.

For homeowners and buyers, even small rate changes can have meaningful financial consequences.

Example:

- $350,000 mortgage at 4% → about $1,670 monthly payment

- Same loan at 7% → about $2,330 monthly payment

That difference can exceed $7,900 per year.

2. Credit Card and Personal Loan Rates

Credit card interest rates respond quickly to Federal Reserve rate changes because most cards are tied to the prime rate, which typically moves with the federal funds rate.

As a result:

- Fed rate increases often lead to higher credit card APRs

- Borrowers carrying balances may see interest costs rise quickly

According to data from the Federal Reserve Bank of St. Louis, average credit card APRs in the U.S. climbed above 20% during recent tightening cycles.

For households with revolving debt, higher interest rates can significantly increase repayment costs.

3. Savings Accounts and CDs

Interest rate increases aren’t always negative for consumers. Savers often benefit when the Federal Reserve raises rates.

Banks typically respond by increasing yields on:

- High-yield savings accounts

- Certificates of deposit (CDs)

- Money market accounts

For example, savings account yields that were below 1% in 2021 rose to 4–5% at many online banks by 2024.

For households holding emergency funds or short-term savings, this change can meaningfully increase interest income.

The Federal Reserve and the Job Market

Another critical way the Federal Reserve affects Americans is through employment.

The Fed’s dual mandate requires balancing inflation with job growth. When the economy overheats and inflation rises too quickly, the Fed may raise interest rates to slow spending and investment.

While this can help stabilize prices, it may also reduce hiring in certain industries.

Conversely, when economic growth slows or unemployment rises, the Fed may lower rates to stimulate economic activity.

This dynamic relationship means Federal Reserve policy often shapes broader economic conditions that influence:

- Hiring trends

- Wage growth

- Business expansion

- Consumer spending

For example, during the COVID-19 recession, the Federal Reserve cut interest rates to near zero and implemented large-scale asset purchases to support economic recovery.

Those policies helped stabilize financial markets and contributed to one of the fastest job market recoveries in modern U.S. history.

Inflation and the Real Cost of Living

Inflation is one of the most important ways the Federal Reserve affects household finances.

When inflation rises rapidly, everyday goods become more expensive.

Common areas where inflation hits household budgets include:

- Groceries

- Gasoline

- Rent and housing

- Healthcare costs

The Fed attempts to keep inflation around 2% annually, a level economists generally consider stable for long-term economic growth.

When inflation rises above that level, the Fed may raise interest rates to reduce demand and slow price increases.

Recent inflation spikes demonstrated how central bank policy influences the cost of living. After inflation surged above 9% in 2022, the Federal Reserve implemented the fastest series of rate hikes in decades to bring price growth under control.

Why Investors Watch the Federal Reserve Closely

Financial markets respond quickly to signals from the Federal Reserve.

Investors analyze:

- FOMC statements

- Economic forecasts

- Speeches from Fed officials

- Interest rate projections

Market reactions can influence retirement accounts, investment portfolios, and pension funds.

Key areas affected include:

- Stock market performance

- Bond yields

- Treasury securities

- Corporate borrowing costs

For Americans saving for retirement through 401(k) plans or IRAs, these shifts can impact long-term portfolio values.

Even small changes in expected interest rates can cause significant movement across global financial markets.

What Happens During a Federal Reserve Meeting?

The Federal Open Market Committee meets about eight times per year to evaluate economic conditions.

During these meetings, policymakers analyze extensive economic data, including:

- Inflation reports

- Employment figures

- Consumer spending trends

- Business investment activity

- Global economic conditions

After reviewing this information, the committee decides whether to:

- Raise interest rates

- Lower interest rates

- Maintain current policy levels

The Fed then releases a public statement explaining its decision and economic outlook.

Financial markets, economists, and businesses analyze this communication carefully because it provides insight into the future direction of monetary policy.

Practical Ways Households Can Respond to Federal Reserve Policy

Although individuals cannot control monetary policy, understanding it can help guide personal financial decisions.

Households often adjust their strategies in response to rate changes.

When interest rates are rising:

- Focus on paying down high-interest debt

- Avoid large adjustable-rate loans if possible

- Lock in fixed mortgage rates when available

When interest rates are falling:

- Consider refinancing mortgages or loans

- Evaluate long-term investment opportunities

- Reassess savings strategies

Understanding the Fed’s policy direction can help households anticipate financial shifts rather than react to them after they occur.

Frequently Asked Questions

1. What exactly does the Federal Reserve do?

The Federal Reserve serves as the central bank of the United States. It manages monetary policy, supervises banks, promotes financial stability, and works to maintain stable prices and maximum employment.

2. How often does the Federal Reserve change interest rates?

The Fed reviews interest rates during scheduled Federal Open Market Committee meetings, typically eight times each year. However, rates may remain unchanged during many of those meetings.

3. Why does the Federal Reserve raise interest rates?

The Fed raises rates primarily to slow inflation. Higher borrowing costs reduce spending and investment, which can help bring price increases under control.

4. Why does the Federal Reserve lower interest rates?

Lower rates encourage borrowing, spending, and investment, helping stimulate economic growth during slowdowns or recessions.

5. Does the Federal Reserve control mortgage rates directly?

No. Mortgage rates are influenced by broader financial markets, particularly Treasury yields, though Federal Reserve policy strongly affects those market conditions.

6. How does the Federal Reserve affect credit card interest rates?

Most credit cards track the prime rate, which usually moves alongside the federal funds rate. When the Fed raises rates, credit card APRs typically increase as well.

7. Who leads the Federal Reserve?

The central bank is led by the Jerome Powell, who serves as Chair of the Federal Reserve Board of Governors.

8. Can Federal Reserve decisions affect unemployment?

Yes. By influencing economic growth through interest rates, the Fed’s policies can indirectly affect hiring trends and unemployment levels.

9. How does the Fed communicate its decisions?

The Federal Reserve releases official statements after policy meetings and holds press conferences to explain economic outlooks and policy decisions.

10. Why do financial markets react so strongly to Federal Reserve announcements?

Markets depend heavily on interest rates and liquidity. Changes in monetary policy can influence borrowing costs, corporate profits, and investment strategies worldwide.

Why Understanding the Fed Helps You Make Smarter Financial Decisions

The Federal Reserve operates behind the scenes, but its policies shape the financial environment Americans live in every day. From borrowing costs to savings returns, and from job opportunities to inflation, the Fed’s decisions ripple across the economy.

For households, understanding these connections offers a practical advantage. It helps people recognize why financial conditions change and how to adapt their personal financial plans accordingly.

Interest rate cycles will continue to influence mortgages, credit cards, investments, and employment trends. By paying attention to Federal Reserve signals and economic conditions, individuals can better prepare for shifts that affect both short-term budgets and long-term financial goals.

Key Points to Remember About the Fed’s Influence

- The Federal Reserve sets monetary policy that affects interest rates across the economy

- Mortgage rates, credit cards, and loans often move in response to Fed decisions

- Higher rates typically slow inflation but increase borrowing costs

- Lower rates encourage economic growth but may raise inflation risks

- Savings yields and investment markets also respond to Fed policy shifts

- Understanding monetary policy can help households make better financial decisions