Summary

The Federal Reserve plays a central role in stabilizing the U.S. economy during downturns. Through tools such as interest rate adjustments, quantitative easing, and financial market interventions, the Fed aims to reduce unemployment, maintain price stability, and restore economic confidence. Understanding how these policies work helps households, investors, and businesses better navigate periods of economic uncertainty.

Understanding the Federal Reserve’s Role in Economic Stability

When the U.S. economy begins to slow—whether due to falling consumer demand, financial instability, or external shocks—the Federal Reserve (often called “the Fed”) becomes one of the most important institutions responding to the situation.

The Federal Reserve is the central bank of the United States, established in 1913 to provide stability to the nation’s financial system. Its mandate, known as the dual mandate, requires it to pursue two primary goals:

- Maximum employment

- Stable prices (low and predictable inflation)

Economic slowdowns threaten both goals simultaneously. Businesses cut back hiring, unemployment rises, and consumer spending weakens. In response, the Federal Reserve uses monetary policy to encourage borrowing, investment, and spending.

The challenge is delicate: act too slowly and the economy can fall into recession; act too aggressively and inflation or financial bubbles may emerge.

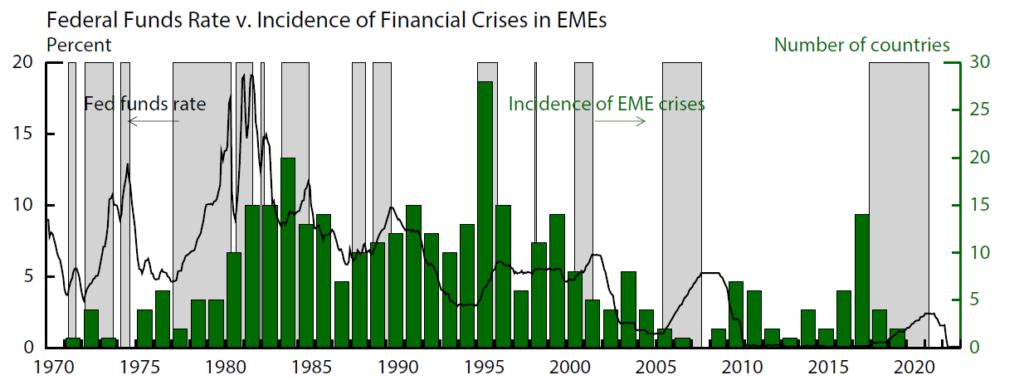

Historically, the Fed has played a decisive role during crises such as the 2008 Global Financial Crisis and the COVID-19 recession in 2020, both of which required rapid policy intervention to stabilize financial markets and restore economic confidence.

How the Federal Reserve Detects an Economic Slowdown

Before the Fed takes action, policymakers analyze a wide range of economic indicators. These signals help determine whether the economy is merely cooling or moving toward recession.

Key indicators the Fed monitors include:

- GDP growth trends

- Unemployment rates and job creation data

- Consumer spending patterns

- Inflation metrics such as the Consumer Price Index (CPI)

- Business investment and manufacturing activity

- Financial market stress indicators

For example, during the early months of the COVID-19 pandemic, unemployment in the United States surged from 3.5% in February 2020 to nearly 15% in April 2020, according to the U.S. Bureau of Labor Statistics. Such rapid deterioration triggered immediate Federal Reserve action.

The Fed’s policy decisions are made by the Federal Open Market Committee (FOMC), which meets roughly eight times per year but can also hold emergency meetings during crises.

Interest Rate Cuts: The Fed’s Primary Tool

The most widely known tool used by the Federal Reserve during economic slowdowns is cutting interest rates.

Specifically, the Fed targets the federal funds rate, which is the rate banks charge each other for overnight lending. When the Fed lowers this rate, borrowing becomes cheaper across the entire economy.

Lower interest rates typically lead to:

- Reduced mortgage rates

- Cheaper auto loans and credit cards

- Lower borrowing costs for businesses

- Increased consumer spending

- Higher business investment

For example, during the 2008 financial crisis, the Federal Reserve cut the federal funds rate from 5.25% in 2007 to nearly zero by late 2008.

This dramatic reduction helped support lending and prevent a deeper collapse in economic activity.

However, interest rate cuts have limits. When rates reach near zero, the Fed must rely on additional tools.

Quantitative Easing: Expanding the Money Supply

When traditional interest rate policy reaches its limits, the Federal Reserve often turns to quantitative easing (QE).

Quantitative easing involves the Fed purchasing large amounts of financial assets—primarily U.S. Treasury securities and mortgage-backed securities—from banks and financial institutions.

The goals of QE include:

- Increasing liquidity in financial markets

- Lowering long-term interest rates

- Encouraging lending and investment

- Supporting housing and credit markets

During the 2008–2014 period, the Federal Reserve purchased trillions of dollars in assets through multiple rounds of QE.

Similarly, in 2020, the Fed launched a massive asset purchase program to stabilize markets during the pandemic-driven economic collapse.

According to Federal Reserve data, the central bank’s balance sheet expanded from roughly $4 trillion in early 2020 to nearly $9 trillion by 2022.

While controversial in some economic circles, QE is widely credited with helping prevent deeper financial system failures.

Emergency Lending and Market Stabilization Programs

In severe economic crises, the Federal Reserve may introduce special lending facilities designed to stabilize specific financial markets.

These programs are intended to ensure that credit continues flowing to businesses, households, and local governments even when private lending markets become unstable.

Examples of emergency programs include:

- Commercial Paper Funding Facility (CPFF) – supports short-term business financing

- Primary Dealer Credit Facility (PDCF) – provides liquidity to major financial institutions

- Municipal Liquidity Facility – supports state and local government borrowing

- Main Street Lending Program – designed to help medium-sized businesses

These programs were heavily used during the 2020 pandemic crisis, when financial markets briefly froze due to uncertainty.

The goal was not to replace private lending but to restore confidence so normal financial activity could resume.

Communication and Forward Guidance

One of the most powerful tools the Federal Reserve uses during economic slowdowns is communication.

Known as forward guidance, this strategy involves publicly signaling the Fed’s future policy intentions to shape expectations among businesses, investors, and consumers.

Forward guidance might include statements such as:

- Interest rates will remain low for an extended period

- The Fed will continue asset purchases until employment improves

- Inflation targets will guide future policy decisions

Clear communication helps financial markets adjust gradually rather than reacting to sudden policy shifts.

For instance, during the COVID-19 recovery, the Fed communicated that rates would remain low until the labor market recovered substantially. This helped maintain stable borrowing conditions.

How Federal Reserve Policies Affect Everyday Americans

Federal Reserve decisions often sound technical, but they have direct impacts on everyday financial life.

When the Fed lowers rates during a slowdown, Americans may experience:

- Lower mortgage rates when buying a home

- Reduced interest on student loan refinancing

- Cheaper business loans for entrepreneurs

- Higher stock market valuations due to lower borrowing costs

For example, during the pandemic recovery period, mortgage rates fell to historic lows—around 2.65% for a 30-year mortgage in early 2021, according to Freddie Mac data.

This triggered a surge in home refinancing and new home purchases.

However, the benefits are not evenly distributed. Savers and retirees relying on fixed income investments may experience lower returns when interest rates remain low.

Challenges and Criticism of Federal Reserve Intervention

Although the Federal Reserve’s actions are designed to stabilize the economy, they are not without controversy.

Some economists argue that aggressive monetary policy can lead to unintended consequences.

Common criticisms include:

- Encouraging excessive risk-taking in financial markets

- Increasing wealth inequality through rising asset prices

- Creating inflationary pressures if stimulus remains too long

- Expanding the Fed’s balance sheet beyond traditional limits

The inflation surge seen in 2021–2022, when U.S. inflation peaked above 9%, reignited debates about whether pandemic-era stimulus policies were too aggressive.

Balancing economic recovery with long-term stability remains one of the most difficult challenges facing central banks.

Lessons from Past Economic Slowdowns

Examining previous downturns reveals important lessons about how the Federal Reserve adapts its strategies.

Key historical episodes include:

The Great Recession (2007–2009)

The Fed introduced quantitative easing and near-zero interest rates to prevent financial collapse.

The COVID-19 Recession (2020)

Rapid rate cuts and massive liquidity programs stabilized financial markets within weeks.

Early 2000s Dot-Com Bust

Interest rate cuts helped cushion the technology sector collapse and supported economic recovery.

These experiences have gradually expanded the Federal Reserve’s toolkit, allowing policymakers to respond more quickly and flexibly during future downturns.

Frequently Asked Questions

1. What does the Federal Reserve do during a recession?

The Fed lowers interest rates, purchases financial assets, and supports lending markets to stimulate economic activity.

2. How do interest rate cuts help the economy?

Lower borrowing costs encourage spending, business investment, and home purchases.

3. What is quantitative easing in simple terms?

It is when the Federal Reserve buys large amounts of government securities to inject money into the financial system.

4. Does the Federal Reserve control inflation?

The Fed influences inflation through interest rates and monetary policy, but it cannot fully control all inflation drivers.

5. How quickly can the Fed respond to a crisis?

The Fed can implement emergency measures within days if necessary, as seen during the 2020 pandemic.

6. Who decides Federal Reserve policy?

The Federal Open Market Committee (FOMC), which includes Federal Reserve Board members and regional bank presidents.

7. Why do stock markets react strongly to Fed decisions?

Interest rates affect corporate borrowing costs, investment flows, and economic growth expectations.

8. Can the Federal Reserve prevent recessions entirely?

No. The Fed can reduce the severity of downturns but cannot eliminate economic cycles.

9. Does the Fed’s policy affect mortgage rates?

Yes. Mortgage rates are strongly influenced by broader interest rate trends shaped by Federal Reserve policy.

10. Why does the Fed sometimes raise rates after a slowdown?

Once the economy recovers, higher rates help prevent inflation and financial imbalances.

Why the Federal Reserve’s Playbook Continues to Evolve

Economic slowdowns are inevitable in a complex, global economy. What matters most is how quickly and effectively policymakers respond.

Over the past several decades, the Federal Reserve has significantly expanded its toolkit—from traditional interest rate policy to unconventional measures such as quantitative easing and emergency lending programs.

These tools have helped stabilize financial markets during some of the most severe economic shocks in modern history.

At the same time, each crisis introduces new challenges. Policymakers must balance the need for rapid intervention with the long-term risks of excessive stimulus.

For businesses, investors, and households, understanding the Fed’s evolving approach provides valuable insight into how economic recoveries take shape.

Key Insights at a Glance

- The Federal Reserve’s dual mandate focuses on employment and price stability

- Interest rate cuts are the Fed’s primary tool during slowdowns

- Quantitative easing helps when rates approach zero

- Emergency lending programs stabilize financial markets during crises

- Fed communication plays a major role in shaping economic expectations

- Monetary policy affects mortgages, business loans, and financial markets

- Balancing stimulus and inflation control remains a major challenge