Summary

Federal Reserve interest rate cycles have repeatedly shaped the U.S. economy, influencing borrowing costs, investment behavior, and financial markets. By examining past tightening and easing cycles—from the inflation battle of the early 1980s to the post-pandemic adjustments—investors, homeowners, and policymakers can better understand how monetary policy works and how rate changes ripple through housing, employment, and markets.

Understanding What a Federal Reserve Rate Cycle Is

A Federal Reserve rate cycle refers to a period in which the U.S. central bank consistently raises or lowers its benchmark interest rate, known as the federal funds rate. These cycles typically occur as policymakers respond to shifts in inflation, employment, economic growth, and financial stability.

The Federal Reserve operates under a dual mandate: maintaining price stability and supporting maximum employment. When inflation rises above the Fed’s target—currently about 2 percent—it often raises interest rates to slow demand. When economic growth weakens or unemployment rises, the Fed may cut rates to stimulate borrowing and spending.

Historically, rate cycles last several months to several years. Their influence spreads through the economy in multiple ways:

- Mortgage rates and home affordability

- Credit card and auto loan interest rates

- Corporate borrowing costs

- Stock and bond market valuations

- Currency strength and global capital flows

Understanding past cycles offers valuable perspective because the Fed’s policy tools and decision-making framework have evolved over decades.

A Quick Look at Major Federal Reserve Rate Cycles

Several rate cycles over the past half century stand out for their economic impact.

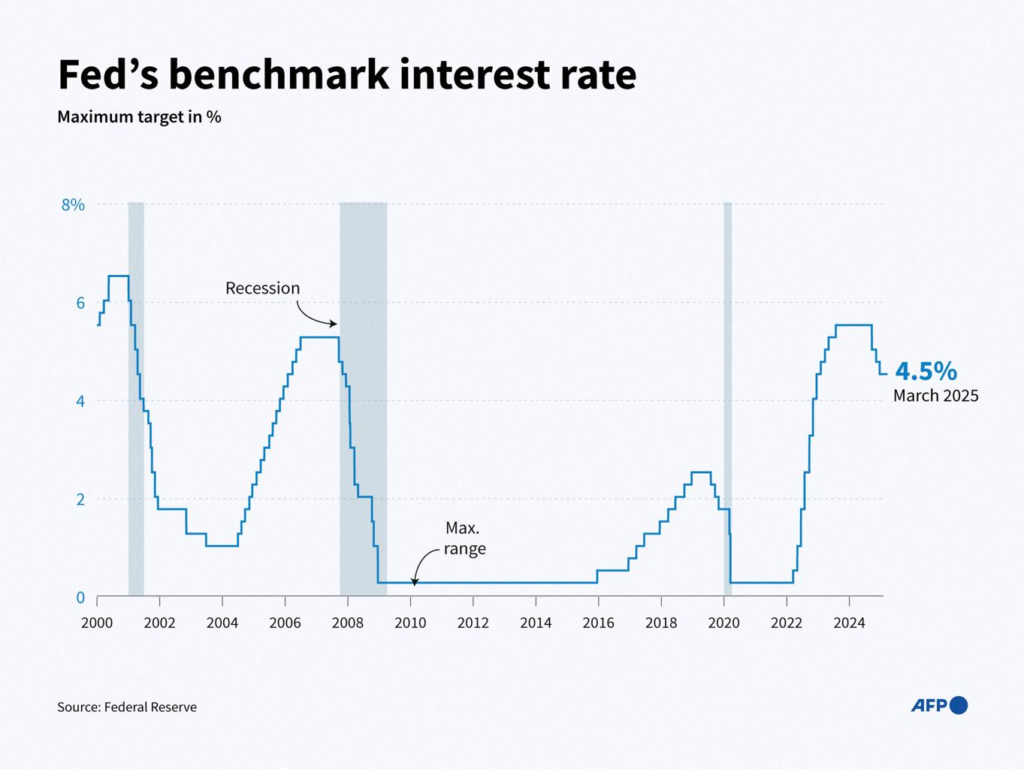

Early 1980s: Fighting Runaway Inflation

In the late 1970s and early 1980s, inflation surged into double digits. Under Federal Reserve Chairman Paul Volcker, the central bank sharply raised interest rates.

The federal funds rate peaked near 20 percent in 1981, the highest level in modern U.S. history.

The result was a deep recession, but inflation eventually fell dramatically. By the mid-1980s, price growth had stabilized, establishing the Fed’s credibility in controlling inflation.

Key lesson: Aggressive rate increases can tame inflation, but often at the cost of economic contraction.

Early 2000s: The Dot-Com Aftermath

After the technology bubble burst in 2000 and the economy weakened, the Federal Reserve lowered interest rates rapidly.

By 2003, the federal funds rate had fallen to 1 percent, helping stabilize economic growth. However, the prolonged period of low rates also contributed to increased risk-taking and the growth of the housing bubble later in the decade.

Key lesson: Extended periods of low rates can stimulate growth but may also encourage excessive borrowing.

2004–2006: Gradual Tightening Before the Financial Crisis

From mid-2004 to mid-2006, the Federal Reserve steadily raised rates from 1 percent to 5.25 percent in a series of small increments.

At the time, policymakers described the increases as moving at a “measured pace.” While the rate hikes were gradual, the housing market had already accumulated significant leverage and risk.

When the housing market weakened in 2007, the financial system proved vulnerable.

Key lesson: Gradual rate increases cannot always prevent asset bubbles from forming.

2008–2015: The Era of Near-Zero Interest Rates

During the global financial crisis, the Federal Reserve reduced the federal funds rate to near zero.

The central bank also introduced quantitative easing, purchasing large amounts of Treasury and mortgage-backed securities to support financial markets.

Rates remained extremely low for several years as the economy slowly recovered.

Key lesson: In severe crises, traditional rate cuts alone may not be enough—unconventional tools become necessary.

2015–2018: The Post-Crisis Normalization

After years of near-zero rates, the Federal Reserve began gradually increasing rates again starting in December 2015.

By 2018, the federal funds rate had reached roughly 2.5 percent. The Fed aimed to normalize policy while avoiding disruption to financial markets.

This cycle demonstrated the difficulty of tightening policy in a highly leveraged global economy.

Key lesson: Even modest rate increases can significantly influence financial markets.

2022–2023: Rapid Tightening to Combat Inflation

Following pandemic-era stimulus and supply disruptions, U.S. inflation surged above 9 percent in 2022.

The Federal Reserve responded with the fastest tightening cycle in decades, raising rates from near zero to over 5 percent within about 18 months.

The pace reflected the urgency of controlling inflation while trying to avoid a deep recession.

Key lesson: Speed of rate hikes can matter as much as the size of the hikes.

Why Rate Cycles Matter for Everyday Americans

Interest rate changes often seem technical, but they directly affect daily financial decisions.

For example, when the Federal Reserve raises rates:

- Mortgage rates typically increase

- Credit card interest rates rise

- Business borrowing becomes more expensive

- Consumer spending may slow

When rates fall, the opposite tends to happen: borrowing becomes cheaper and economic activity often accelerates.

A homeowner considering refinancing, a small business planning expansion, or an investor managing a portfolio all feel the effects of these policy shifts.

Patterns That Appear Across Rate Cycles

Looking across decades of Federal Reserve decisions reveals several consistent patterns.

Monetary Policy Works With a Time Lag

Economic effects rarely appear immediately.

It can take 6–18 months for rate changes to fully influence inflation, employment, and consumer spending.

For example, the aggressive rate hikes of the early 1980s triggered recession only after months of tightening.

This lag complicates policymaking because the Fed must anticipate future conditions rather than reacting solely to current data.

Financial Markets Often Move Ahead of the Fed

Investors frequently anticipate rate changes before they occur.

Bond yields, stock valuations, and currency markets may shift months ahead of official policy moves as traders interpret economic data and Federal Reserve communication.

For instance, Treasury yields often rise in advance of tightening cycles when markets expect inflation or stronger growth.

Housing Is Especially Sensitive to Interest Rates

Among all sectors of the economy, housing tends to respond quickly to rate changes.

Higher mortgage rates can significantly reduce affordability for buyers. A one-percentage-point increase in mortgage rates can raise monthly payments by hundreds of dollars.

As a result, housing activity often slows during tightening cycles and rebounds when rates fall.

Rate Cycles Are Rarely Perfectly Timed

Even with extensive economic research and data, policymakers cannot always predict turning points.

Some cycles end earlier than expected due to unexpected events such as:

- Financial crises

- Energy price shocks

- Global recessions

- Banking instability

Because of this uncertainty, Federal Reserve officials often emphasize a data-dependent approach.

Lessons Investors Often Draw From Rate Cycles

Investors study historical rate cycles carefully because interest rates influence asset prices.

Some practical observations that frequently appear in investment research include:

- Bond prices usually fall when rates rise

- Growth stocks can be sensitive to higher interest rates

- Bank profitability sometimes improves during moderate rate increases

- Dividend-paying stocks often become less attractive when bond yields rise

However, markets rarely move in a perfectly predictable pattern. Other factors—corporate earnings, global economic trends, and investor sentiment—also play important roles.

Lessons for Homebuyers and Borrowers

For individuals considering major financial decisions, past rate cycles highlight several useful principles.

First, borrowing costs can change rapidly. Mortgage rates may rise or fall significantly within a year during active rate cycles.

Second, waiting for the perfect interest rate can be difficult because markets often move unpredictably.

Finally, affordability matters more than the absolute rate level. Many buyers in the 1980s purchased homes despite double-digit mortgage rates because home prices were significantly lower relative to incomes.

The broader lesson is that financial planning should account for changing interest rate environments.

How the Federal Reserve Communicates Policy Today

One major difference between earlier rate cycles and modern ones is greater transparency.

Today the Federal Reserve regularly publishes:

- Meeting minutes

- Economic projections

- Press conference statements

- Policy guidance

This communication strategy aims to reduce market surprises and help households and businesses plan for potential policy changes.

Clear communication has become a key tool of modern monetary policy.

What the Future May Hold for Rate Cycles

While every economic environment is different, several structural factors are likely to influence future cycles.

These include demographic shifts, global trade dynamics, government debt levels, and technological change.

Many economists believe that long-term interest rates may remain lower than historical averages due to aging populations and high global savings.

However, unexpected inflation shocks—like those seen in 2022—can still trigger rapid policy tightening.

History suggests that rate cycles will continue to evolve alongside economic conditions.

Frequently Asked Questions

What triggers a Federal Reserve rate cycle?

Rate cycles typically begin when inflation rises above target levels or when economic growth weakens significantly.

How often does the Federal Reserve change interest rates?

The Fed meets eight times per year, but rate changes do not occur at every meeting.

How long does a typical rate cycle last?

Some cycles last less than a year, while others extend over several years depending on economic conditions.

Do Federal Reserve rate hikes always cause recessions?

No. While some tightening cycles have preceded recessions, others have resulted in slower but still positive economic growth.

Why do markets react so strongly to Fed announcements?

Interest rates affect nearly every financial asset, so even small policy shifts can influence valuations.

How quickly do mortgage rates respond to Fed policy?

Mortgage rates often move in anticipation of Fed policy changes, sometimes weeks or months before official decisions.

What is the federal funds rate?

It is the interest rate banks charge each other for overnight lending and serves as the primary benchmark for U.S. monetary policy.

Can the Fed control inflation immediately?

No. Policy changes affect the economy gradually due to delayed responses in spending, investment, and employment.

Why did the Fed keep rates near zero after the 2008 crisis?

The economy required significant support after the financial crisis, and low rates helped stimulate borrowing and investment.

Are rate cycles predictable?

Economists can identify trends, but precise timing is difficult due to unpredictable economic events.

The Enduring Influence of Monetary Policy Cycles

Federal Reserve rate cycles reveal how closely monetary policy and economic behavior are intertwined. From the inflation battle of the 1980s to the rapid tightening of the early 2020s, each cycle reflects the economic challenges of its time.

The most consistent lesson is that interest rates shape decisions across the entire economy—from household mortgages to corporate investments. While no cycle unfolds exactly like the last, understanding the patterns behind past policy decisions helps individuals, businesses, and investors navigate future economic shifts with greater perspective.

Key Insights From Past Rate Cycles

- Interest rate changes influence the economy with significant time delays

- Financial markets often anticipate Federal Reserve actions

- Housing markets are especially sensitive to rate changes

- Prolonged low rates can encourage risk-taking

- Rapid tightening can slow inflation but also pressure growth

- Monetary policy works best when paired with clear communication