Summary

Over the past century, the Federal Reserve has transformed from a modest banking stabilizer into one of the world’s most influential economic institutions. Created in response to financial crises, the Fed now guides interest rates, supervises banks, manages inflation, and supports financial stability. Understanding how its responsibilities expanded helps explain how monetary policy shapes borrowing costs, employment, and the broader U.S. economy today.

Introduction: Why the Federal Reserve Matters More Than Ever

The Federal Reserve, often called “the Fed,” plays a central role in the U.S. financial system. It influences interest rates, oversees banks, manages the nation’s money supply, and responds to financial crises. Yet the Fed’s responsibilities today are far broader than when it was created in 1913.

Over the past century, a series of economic shocks—including the Great Depression, World War II, the inflation crises of the 1970s, the 2008 financial crisis, and the pandemic-era recession—reshaped the Fed’s powers and tools. Each moment forced policymakers to rethink how central banking should work in the United States.

Today, the Federal Reserve’s decisions affect everything from mortgage rates and credit cards to global financial markets. Understanding how its role evolved helps Americans better interpret interest rate announcements, inflation reports, and economic forecasts.

The Origins of the Federal Reserve (1913–1930s)

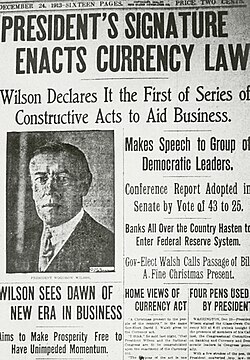

The Federal Reserve System was established through the Federal Reserve Act of 1913 after decades of financial instability. Before its creation, the United States experienced frequent banking panics. The Panic of 1907, in particular, exposed weaknesses in the country’s decentralized banking system.

At that time, there was no central authority to provide emergency liquidity when banks ran short of cash. The Fed was designed to fill that gap.

Originally, the institution focused on three main goals:

- Acting as a lender of last resort during banking crises

- Providing a more stable and flexible currency supply

- Supporting the functioning of the national banking system

The structure of the Fed reflected American skepticism toward centralized power. Instead of one national bank, it included 12 regional Federal Reserve Banks overseen by a central governing board in Washington, D.C.

However, the Fed’s early years revealed limitations. During the Great Depression of the 1930s, thousands of banks failed and unemployment surged above 20%. Many historians argue that the Fed did not respond aggressively enough to stabilize the banking system.

That crisis ultimately reshaped the institution’s mission.

Lessons from the Great Depression

The economic devastation of the 1930s forced Congress to reconsider how monetary policy should work.

Major legislative reforms during this period included:

- The Banking Act of 1933, which created federal deposit insurance through the FDIC

- The Banking Act of 1935, which strengthened the Federal Reserve Board and centralized decision-making

- Expanded authority over monetary policy and financial stability

One of the key lessons from the Great Depression was the importance of stabilizing the money supply. Economists later argued that allowing the banking system to collapse worsened the downturn.

These reforms helped shift the Federal Reserve from a passive institution into a more active manager of economic stability.

The Post-War Era and the Rise of Modern Monetary Policy

After World War II, the Federal Reserve entered a new phase. The U.S. economy was expanding rapidly, global trade was growing, and financial markets were becoming more complex.

In 1951, the Treasury–Federal Reserve Accord gave the Fed greater independence from the U.S. Treasury. Before this agreement, the Fed was effectively required to keep interest rates low to help finance government debt during the war.

The accord allowed the Federal Reserve to pursue monetary policy focused on economic stability rather than government financing needs.

Over the next several decades, the Fed increasingly relied on interest rate adjustments to influence economic activity. By raising or lowering short-term interest rates, policymakers could influence borrowing, spending, and investment.

For example:

- Lower rates typically encourage borrowing and economic growth

- Higher rates help slow inflation and excessive spending

This approach became the foundation of modern central banking.

The Inflation Crisis of the 1970s

The 1970s marked one of the most difficult periods in the Federal Reserve’s history. The United States experienced stagflation, a rare combination of high unemployment and high inflation.

Oil price shocks, rising wages, and loose monetary policy contributed to inflation that exceeded 13% in 1979.

To address the crisis, Federal Reserve Chair Paul Volcker implemented aggressive interest rate increases beginning in 1979. The federal funds rate climbed above 19% at one point.

The policy triggered a deep recession but ultimately succeeded in reducing inflation.

This period reinforced the Fed’s commitment to controlling inflation as a central priority. It also demonstrated that monetary policy decisions sometimes require difficult tradeoffs between short-term economic pain and long-term stability.

The Federal Reserve’s Dual Mandate

In 1977, Congress formally clarified the Federal Reserve’s goals through an amendment to the Federal Reserve Act.

The Fed’s dual mandate requires it to pursue:

- Maximum employment

- Stable prices

In practice, this means balancing job growth with inflation control. Policymakers analyze a wide range of data, including unemployment rates, wage growth, consumer prices, and economic output.

The dual mandate continues to guide Federal Reserve decision-making today.

The Global Financial Crisis and Expanded Powers

The 2008 financial crisis marked another turning point in the Fed’s evolution. As housing markets collapsed and financial institutions faced insolvency, the Federal Reserve took unprecedented steps to stabilize the economy.

Key actions included:

- Reducing interest rates to near zero

- Launching quantitative easing (QE) programs to purchase government bonds and mortgage-backed securities

- Providing emergency liquidity to banks and financial institutions

Quantitative easing dramatically expanded the Fed’s balance sheet—from under $1 trillion before the crisis to more than $4 trillion in the following years.

Congress also passed the Dodd–Frank Act of 2010, which expanded the Fed’s responsibilities for financial regulation and systemic risk oversight.

This period cemented the Federal Reserve’s role not only as a monetary authority but also as a guardian of financial stability.

The Pandemic Era and New Policy Tools

The economic shock caused by the COVID-19 pandemic in 2020 required another extraordinary response.

The Federal Reserve quickly introduced multiple emergency programs designed to stabilize credit markets and support economic recovery.

Among the major actions:

- Cutting interest rates back to near zero

- Purchasing trillions of dollars in Treasury securities

- Creating lending facilities for businesses, municipalities, and financial markets

These policies helped maintain liquidity across the financial system during a period of extreme uncertainty.

At the same time, the Fed introduced a revised policy framework emphasizing average inflation targeting, allowing inflation to temporarily exceed its 2% target following periods of low inflation.

How the Federal Reserve Influences Everyday Financial Life

While the Federal Reserve operates behind the scenes, its policies directly affect many aspects of daily financial life.

Examples include:

- Mortgage interest rates

- Credit card APRs

- Auto loan financing

- Savings account yields

- Stock and bond market performance

For instance, when the Fed raises interest rates to combat inflation, borrowing costs for mortgages and credit cards typically increase as well. When it lowers rates, borrowing becomes cheaper and economic activity often rises.

This is why financial markets—and millions of American households—pay close attention to Federal Reserve announcements.

Why the Fed’s Role Continues to Evolve

The Federal Reserve’s responsibilities continue to expand as financial systems grow more complex. Policymakers are increasingly focused on emerging challenges such as:

- Financial system resilience

- Digital payment systems

- Global economic integration

- Rapid technological change in financial markets

Central banks around the world are also studying central bank digital currencies (CBDCs), though the United States has not yet adopted one.

What remains constant is the Fed’s core mission: maintaining economic stability in a rapidly changing financial environment.

Frequently Asked Questions

What is the main purpose of the Federal Reserve?

The Federal Reserve aims to promote stable prices, maximum employment, and financial system stability through monetary policy and bank supervision.

Who controls the Federal Reserve?

The Federal Reserve operates independently within government. Its Board of Governors is appointed by the President and confirmed by the Senate.

How does the Federal Reserve influence interest rates?

The Fed adjusts the federal funds rate, which influences borrowing costs across the banking system and the broader economy.

What is the federal funds rate?

It is the interest rate banks charge each other for overnight loans, serving as a benchmark for many other interest rates.

Why was the Federal Reserve created?

The Fed was created after repeated financial panics to stabilize the banking system and provide emergency liquidity.

What is quantitative easing?

Quantitative easing is a policy where the Fed purchases government bonds or other securities to increase money supply and lower long-term interest rates.

How often does the Federal Reserve meet?

The Federal Open Market Committee (FOMC) typically meets eight times per year to evaluate economic conditions and adjust policy.

Can the Federal Reserve control inflation?

The Fed cannot directly control prices but can influence inflation by adjusting interest rates and managing the money supply.

Why does the Fed raise interest rates?

Rates are typically increased to slow inflation and prevent the economy from overheating.

Does the Federal Reserve print money?

The U.S. Treasury prints physical currency, but the Fed controls the money supply through monetary policy and financial system operations.

Looking Ahead: The Federal Reserve’s Continuing Influence

A century after its creation, the Federal Reserve remains one of the most influential institutions shaping the U.S. economy. Its responsibilities have expanded from stabilizing banks to guiding monetary policy, supervising financial institutions, and responding to global economic shocks.

Future challenges—from technological change to evolving financial markets—will likely continue to reshape how the Fed operates. Yet its central mission remains unchanged: promoting a stable and resilient economy.

Key Points to Remember

- The Federal Reserve was created in 1913 to stabilize the banking system

- The Great Depression expanded its authority and reshaped monetary policy

- The dual mandate focuses on employment and inflation stability

- Major crises, including 2008 and 2020, broadened the Fed’s role further

- Federal Reserve decisions influence borrowing costs, markets, and economic growth

- Its policies affect everyday finances, from mortgages to savings rates