Tax cuts have always been one of the most debated topics in U.S. economic and political circles. Supporters argue that tax cuts stimulate economic growth, boost investment, and leave more money in the hands of consumers and businesses. Critics, on the other hand, warn that lowering taxes can reduce government revenues, increase deficits, and undermine the ability of the federal government to fund essential programs. In 2025, with the U.S. economy facing inflationary pressures, rising debt levels, and evolving global competition, the impact of tax cuts on federal revenues has become even more relevant.

This article explores how tax cuts influence federal revenues, looking at both the short-term and long-term effects, the historical context, and the current implications for the U.S. economy.

Understanding Federal Revenues

Federal revenues primarily come from three sources: individual income taxes, corporate taxes, and payroll taxes. Individual income taxes account for the largest share, while corporate taxes and payroll contributions make up the rest. Any change in tax policy—such as lowering corporate tax rates or adjusting personal income tax brackets—directly impacts the flow of money into the federal treasury.

When tax cuts are introduced, federal revenues typically decline in the short run. The extent of this decline depends on the size of the cuts, the groups targeted, and the state of the economy. For example, a broad cut in personal income taxes reduces the amount collected from households, while corporate tax cuts shrink contributions from businesses.

The Argument for Tax Cuts Boosting Growth

One of the main justifications for tax cuts is rooted in supply-side economics. The idea is that when individuals and corporations keep more of their income, they spend and invest more. This can create new jobs, drive innovation, and expand the overall tax base. Proponents believe that the resulting economic growth eventually compensates for the initial loss in revenue.

For instance, if a company pays less in corporate taxes, it might use the savings to expand operations, hire more workers, or increase wages. Those workers then pay income taxes and spend money, generating more sales tax revenues at the state level and stimulating economic activity nationwide.

However, the question remains: does this growth offset the decline in direct federal tax collections? The answer depends on multiple factors, including the structure of the tax cuts, consumer behavior, and overall economic conditions.

Historical Lessons: The Reagan and Bush Tax Cuts

To understand the impact of tax cuts on federal revenues, it helps to examine history. During the 1980s, President Ronald Reagan introduced significant tax reductions. Supporters hailed the reforms for encouraging investment and spurring growth. However, federal revenues initially declined, and budget deficits surged, leading to concerns about fiscal sustainability.

Similarly, in the early 2000s, President George W. Bush signed into law a series of tax cuts designed to stimulate the economy after the dot-com bubble burst and the September 11 attacks. While the cuts provided short-term relief for households and businesses, they also contributed to rising federal deficits.

In both cases, the promise that tax cuts would “pay for themselves” did not fully materialize. Although the economy experienced periods of growth, the growth was not sufficient to completely offset the revenue losses.

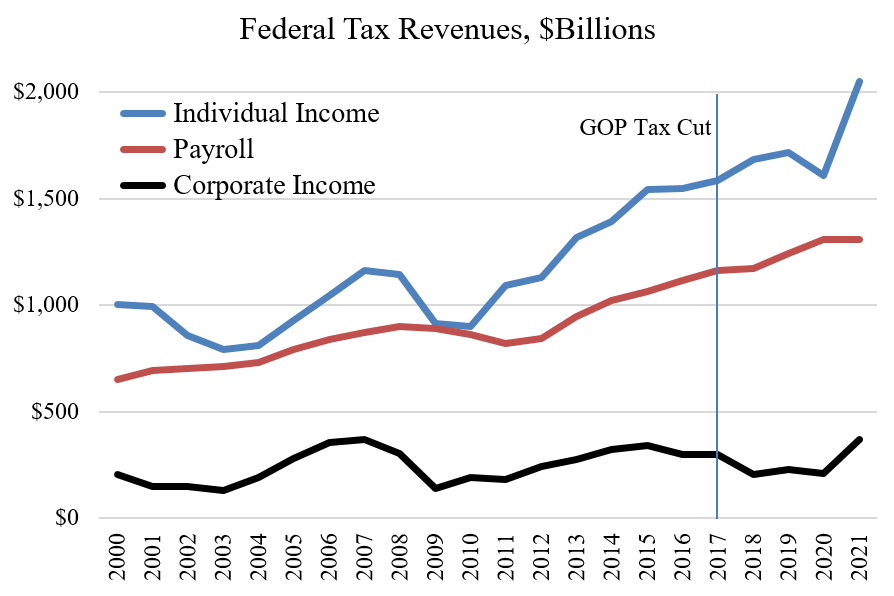

The Trump Era Tax Cuts and Jobs Act (TCJA)

The most recent major tax reform came in 2017 under President Donald Trump with the Tax Cuts and Jobs Act (TCJA). The law lowered the corporate tax rate from 35% to 21% and provided temporary relief for individuals through changes in deductions and lower rates.

Supporters argued that the corporate tax reduction made U.S. businesses more competitive globally and encouraged companies to bring profits back from overseas. Critics noted that while some companies reinvested savings, others used the extra money primarily for stock buybacks, benefiting shareholders more than workers.

From a revenue perspective, the Congressional Budget Office (CBO) estimated that the TCJA significantly reduced federal revenues. While economic growth did improve in 2018 and 2019, it was not enough to offset the revenue shortfall, contributing to higher federal deficits.

The Current Landscape in 2025

In today’s environment, the debate over tax cuts continues. Some policymakers advocate extending or expanding certain provisions of the TCJA, while others call for rolling them back to raise revenues. At the same time, the U.S. faces challenges such as servicing a large national debt, funding Social Security and Medicare, and investing in infrastructure and climate initiatives.

Federal revenues have been constrained by past tax cuts, even as spending commitments have grown. The mismatch between revenues and expenditures raises questions about long-term fiscal stability. While economic growth has partially cushioned the impact, it has not fully eliminated the structural deficits created by reduced tax collections.

Do Tax Cuts Always Lead to Lower Revenues?

It is important to note that the relationship between tax cuts and revenues is not always straightforward. In some cases, especially when tax rates are very high, cutting rates can actually increase compliance and reduce tax avoidance, leading to stable or even higher revenues. This concept, known as the Laffer Curve, suggests that there is an optimal tax rate that maximizes government revenues without discouraging economic activity.

However, in practice, the U.S. tax rates in recent decades have not been high enough for this effect to dominate. Most analyses show that large-scale tax cuts tend to reduce revenues, even if they spur growth.

The Impact on Deficits and Debt

Reduced federal revenues from tax cuts often translate into larger budget deficits unless offset by spending cuts. Deficits, in turn, contribute to the national debt. This dynamic has significant implications for future generations, as higher debt requires more interest payments and limits the government’s fiscal flexibility.

Critics argue that tax cuts, especially those benefiting the wealthy and corporations, deepen inequality while straining public finances. Proponents counter that economic growth generated by tax cuts benefits everyone and that long-term debt concerns can be addressed separately through spending reforms.

Balancing Growth and Fiscal Responsibility

The key challenge for U.S. policymakers is finding a balance between encouraging growth and maintaining fiscal responsibility. Tax policy is a powerful tool that can shape economic incentives, but it also directly affects the government’s ability to provide essential services.

Future tax reforms may focus on targeted relief—such as credits for middle-income families, incentives for green investments, or adjustments to capital gains taxes—rather than broad-based cuts. Such targeted measures might provide economic benefits while minimizing revenue losses.

Conclusion

The impact of U.S. tax cuts on federal revenues is complex and depends on the structure of the cuts, the state of the economy, and long-term fiscal policies. Historical experience suggests that while tax cuts can stimulate growth, they rarely generate enough new revenue to fully compensate for the loss in tax collections.

As the U.S. navigates the challenges of 2025 and beyond, policymakers must carefully weigh the benefits of tax cuts against the risks of higher deficits and growing debt. The ultimate question is not just whether tax cuts reduce revenues, but whether the economic and social gains they create are worth the fiscal trade-offs.